If you make your monthly payment precisely on your due date, you'll pay the specific quantity of interest that you had initially prepared. However, if you make a payment prior to your due date, less interest will accumulate, so more of your fixed Get more information payment will go towards the principal. On the other side, if you make your payment late, more interest will accrue, so more of your payment will go towards interest and less towards principal.

9% Repaired regular monthly payment is $386 Your daily financing charge would be computed as follows: ($ 20,000 x 5. 9%)/ 365 days each year = $3. 23/day If your $386 payment is received exactly 1 month from the date of your last payment, your financing charge for that duration would be $96.

23 x 30 days). Your $386 payment would be divided in between primary and the financing charge: Principal: $289. 10 Finance Charge: $96. 90 Overall: $386. 00 If you make your next payment exactly one month later, the primary amount would be greater and the financing charge would be lower. If you have extra concerns, please contact our Loan Department at (800) 749-9732 ext.

If you're going to be accountable for paying a mortgage for the next 30 years, you must know exactly what a mortgage is. A home loan has three fundamental parts: a deposit, month-to-month payments and fees. Because home mortgages usually include a long-term payment strategy, it's essential to understand how they work.

is the quantity required to settle the home loan over the length of the loan and includes a payment on the principal of the loan as well as interest. There are often residential or commercial property taxes and other costs included in the monthly bill. are numerous expenses you have to pay up front to get the loan.

Some Known Incorrect Statements About How Does The Trump Tax Plan Affect Housing Mortgages

The larger your deposit, the much better your funding deal will be. You'll get a lower home loan interest rate, pay less costs and gain equity in your house more rapidly. Have a great deal of concerns about home loans? Take a look at the Customer Financial Defense Bureau's responses to regularly asked concerns. There are 2 primary kinds of home mortgages: a standard loan, ensured by a private lender or banking organization and a government-backed loan.

This eliminates the requirement for a deposit and likewise prevents the need for PMI (private mortgage insurance coverage) requirements. There are programs that will assist you in obtaining and financing a home loan. Check with your bank, city advancement office or an educated real estate representative to discover more. The majority of government-backed home mortgages can be found in among 3 forms: The U.S.

The primary step to get a VA loan is to acquire a certificate of eligibility, then submit it with your latest discharge or separation release documents to a VA eligibility center. The FHA was produced to assist individuals obtain economical real estate (what act loaned money to refinance mortgages). FHA loans are actually made by a loaning organization, such as a bank, however the federal government guarantees the loan.

Backed by the U.S. Department of Agriculture, USDA loans are for rural property purchasers who are without "good, safe and sanitary housing," are unable to protect a home mortgage from standard sources and have an adjusted income at or below the low-income limit for the location where they live. After you pick your loan, you'll decide whether you desire a repaired or an adjustable rate.

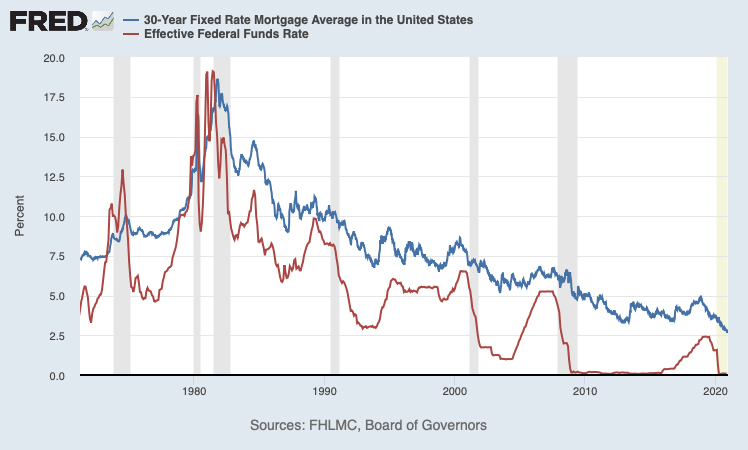

A fixed rate home loan needs a monthly payment that is the very same quantity throughout the regard to the loan. When you sign the loan papers, you settle on a rates of interest which rate never changes. This is the finest kind of loan if rates of interest are low when you get a mortgage.

The What Are The Types Of Reverse Mortgages Diaries

If rates go up, so will your home mortgage rate and month-to-month payment. If rates increase a lot, you could be in big problem. If rates go down, your home mortgage rate will drop and so will your monthly payment. It is normally best to stick with a fixed rate loan to secure against rising rate of interest.

The quantity of cash you obtain affects your rates of interest. Mortgage sizes fall into 2 main size classifications: conforming and nonconforming. Conforming loans fulfill the loan limit guidelines set by government-sponsored mortgage associations Fannie Mae and Freddie Mac. Non-conforming loans include those made to customers with poor credit, high financial obligation or recent personal bankruptcies.

If you want a house that's priced above your regional limitation, you can still qualify for an adhering loan if you have a big enough deposit to bring the loan amount down listed below the limit. You can reduce the rates of interest on your home mortgage loan by paying an up-front cost, called home mortgage points, which subsequently minimize your monthly payment.

125 percent. In this method, buying points is said to be "purchasing down the rate." Points can likewise be tax-deductible if the purchase is for your main residence. If you plan on living in your next home for at least a decade, then points may be a great option for you.

Within 3 days after receiving your loan application, a home loan service provider is required to give you a good-faith quote (GFE) that details all the charges, fees and terms associated with your home loan. Your GFE likewise includes an estimate of the overall you can expect to pay when you close on your house.

The Best Strategy To Use For What Are The Percentages Next To Mortgages

If your loan is denied within http://holdeniisb663.bravesites.com/entries/general/top-guidelines-of-which-of-the-following-statements-is-not-true-about-mortgages 3 days, then you are not guaranteed a GFE, however you do can request for and get the particular reasons your loan was denied. The interest rate that you are priced quote at the time of your mortgage application can alter by the time you sign your home mortgage.

This guarantee of a fixed rate of interest on a mortgage is only possible if a loan is closed in a specified time period, typically 30 to 60 days. The longer you keep your rate lock past 60 days, the more it will cost you. Rate locks can be found in different forms a percentage of your home mortgage quantity, a flat one-time cost, or merely an amount figured into your interest rate.

While rate locks Helpful resources generally avoid your interest rate from increasing, they can also keep it from going down. You can look for loans that offer a "drift down" policy where your rate can fall with the marketplace, however not rise. A rate lock is worthwhile if an unforeseen increase in the interest rate will put your mortgage out of reach.

The PMI protects the lending institution's liability if you default, enabling them to release home loans to someone with lower down payments. The cost of PMI is based on the size of the loan you are obtaining, your deposit and your credit rating. For instance, if you put down 5 percent to acquire a home, PMI might cover the additional 15 percent.

As soon as your home loan principal balance is less than 80 percent of the original assessed worth or the current market price of your home, whichever is less, you can generally cancel the PMI. Your PMI can likewise end if you reach the midpoint of your benefit for example, if you secure a 30-year loan and you total 15 years of payments.